July 18th, 2022

In Summary

- Total new home sales among the 50 Top-Selling Master-Planned Communities declined by 18% in the first half of 2022 compared to the same time period last year.

- Supply chain issues and inadequate new home inventory have continued to pose problems for builders, and price increases and interest rate hikes have begun to impact traffic from potential buyers in recent months.

- Nationally, the average price among all new single-family homes is up 15% since Mid-Year 2021, and over 40% since April 2020 and the depths of pandemic pricing.

- The Villages active-adult community is once again the top-selling community in the nation with an estimated 1,500 sales year to date.

- Sarasota, Florida’s Lakewood Ranch claimed the number two spot overall, and is the top-selling multi-generational community in the country, with 1,026 sales.

- Dallas, Texas’s Silverado has earned the third-place rank through the first half of the year with 599 sales.

- Houston, Texas’s Sunterra, and Southwest Florida’s Babcock Ranch each ranked within the Top-10 for the first time with a strong performance to start the year.

- The Houston MSA was the top-performing metropolitan area with 13 communities in the Top-50, representing 3,430 sales, or almost 20% of all sales among ranked MPCs.

- The state of Florida represented about 36% of sales among ranked communities, followed closely by Texas at nearly 34%.

Every year since 1994, RCLCO has conducted a national survey identifying the top-selling master-planned communities (MPCs) through a rigorous search of high-performing communities in each state. Each year we report the annual sales among the Top-50 communities at the end of the year, as well as publish this mid-year update report each July. For this mid-year 2022 report, we have surveyed MPCs throughout the country to establish the current rankings as an update to our Top-Selling Master-Planned Communities of 2021.

The chart above summarizes RCLCO’s list of the 50 top-selling communities through the first half of 2022, including a comparison with their home sales through the first half of 2021 where applicable. Sales among the Top-50 communities of Mid-Year 2022 declined by 18% compared to the pace set in the first half of 2021, with developers continuing to cite supply chain issues and a lack of inventory, along with instances of declining traffic from potential buyers in more recent months as high prices and interest rate hikes continue to have an impact on consumer’s purchasing power. The Villages, an active adult community in Central Florida, is once again the top-selling community in the country with an estimated 1,500 sales. Sarasota, Florida’s Lakewood Ranch claims the top spot among all-ages communities, with 1,026 sales. Dallas, Texas’s Silverado has earned the third-place rank through the first half of the year with 599 sales. Sunterra, located in Houston, Texas, ranked within the Top-10 for the first time this year due to a strong performance in the first half of 2022 that resulted in an eight place finish. Babcock Ranch, located in Southwest Florida, also entered the Top-10 for the first time, with a 14% increase in sales pace compared to the first half of 2021.

Top-Selling Master-Planned Communities of Mid-Year 2022

In our Year-End 2021 issue of RCLCO’s Top-Selling Master-Planned Communities Report, we reported that sales among Top-Selling communities increased modestly in the first half of the year before slowing in the second half of 2021. Supply chain disruptions, labor market tightness, and cost surges were among the most cited reasons for that modest growth in 2021 sales, though optimism remained strong for 2022 as demand remained strong and market participants hoped for the timely resolution of supply chain woes. That optimism was not rewarded and the slowing pace of new single-family home sales has continued through May of 2022, according to the most recent data available. Now, rising mortgage rates, which have gone up 2% since the beginning of the year, indicate the softening we have seen in the new home market may yet continue. With mortgage rates likely to remain in the 6%+/- range for the rest of the year and inflation still high, along with recession fears and low consumer confidence, housing demand is likely to cool still further in the short term.

Despite this potential cooling, attitudes among Master-Planned Community developers remain optimistic, and there are numerous reasons why this should be the case. For one, while many consumers have been priced out of the new home market by rising mortgage rates and prices, pent-up demand from the remaining new home buyers is still substantial. The current situation of slowing sales might therefore be viewed as more of a “pause” as consumers get used to higher rates. In some instances, builders have even been noted as viewing this “pause” as more of a silver lining – using the period of slowing sales as an opportunity to catch-up on closings and build-up on inventory.

More on the Top-Selling Master-Planned Communities

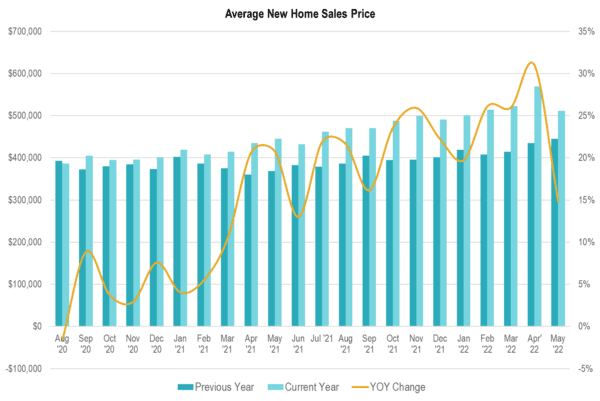

Despite slowing of new sales, many developers have remained optimistic since higher prices have meant that they’ve been able to meet budget despite fewer sales. Nationally, the price of a new single family home is up 15% since last year, and up over 40% since the start of the pandemic, as shown in the table below.

Source: RCLCO

Source: RCLCO

Many MPCs have experienced increases in average new home prices greater than the market overall. For example, Lakewood Ranch reported new home price appreciation of 47% over the past year, while the regional average grew by just 22%.

“In my opinion, the Sarasota market and Lakewood Ranch in particular were undervalued as a primary home location prior to the pandemic. ‘Live where you vacation’ became a driving decision for many homebuyers, and I don’t see that trend reversing or being less valued. We offer that in spades in Lakewood Ranch and the Tampa Bay region.”

– Laura Cole, Senior Vice President at Lakewood Ranch

Despite the near term slowing of new home sales in MPC’s and the market overall, the fundamentals underlying new home demand for the longer term remain strong. Specifically, as millennial households continue to enter their prime family formation years in large numbers, a life stage that traditionally precedes single-family home ownership, long-term demand for single-family housing is likely to remain strong. Furthermore, these strong demand projections brought on by demographic tailwinds are coupled with a housing environment that continues to be undersupplied. If there is a recession, as some economists are predicting, it’s important to remember that on average, in past recessions new home sales declined by less than 10% – except when they fell a whopping 66% in the first year of the 2008 recession, under very different circumstances. While a recession may result from the Federal Reserve raising interest rates in order to combat inflation, the housing market is not oversupplied the way it was in 2008.

Master-Planned Communities: Safety in Times of Recession

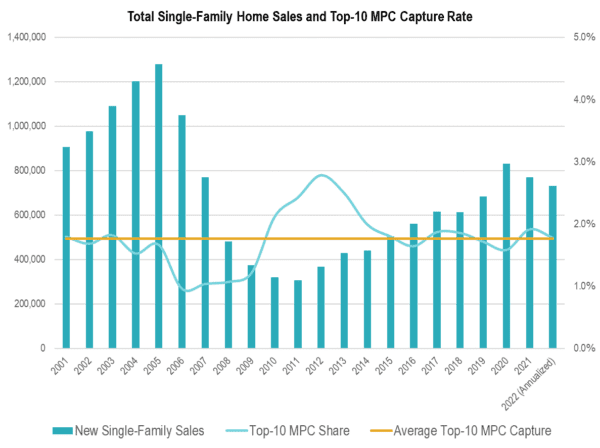

There remains an additional silver lining for master-planned community developers in the context of concerns about a possible recession. Historically, Master-Planned Communities have tended to increase their market share in times of economic turmoil, as shown in the graph below which compares sales in the Top-10 master-planned communities in the country to overall new sales from 2001 to 2022. During the run-up to the Great Recession, as an example, MPC market share fell, then significantly increased when overall sales in the market fell. This is an example of the “flight to quality” and perhaps a “flight to safety” wherein MPCs are perceived as a better, safer investment as well as place to live in challenging economic periods.

Source: RCLCO

Source: RCLCO

Market Outlook: Long-Term Strength of Housing Demand

Precisely when and how severe the next recession will be is impossible to predict. The technical definition of a recession is two consecutive quarters of negative economic growth as measured by GDP, although the National Bureau of Economic Research (NBER) takes other factors into account in calling recessions. In the last 7 recessions, the timing and impact of the recession on residential real estate depended on the economic and political circumstances of the particular time period. Rising prices and mortgage rates have contributed to declining housing affordability, and the potential exists for short-term declines in permitting, starts and new home sales. Given the underlying demographic trends supporting long-term new housing demand, permits, starts, and new home sales will likely rebound substantially following a recession if there is one, perhaps by mid to late 2023, although timing is impossible to predict. The exact timing of any rebound depends on if, and when, a recession occurs. Meanwhile it’s important to recognize that the current slowing is a short-term trend, and the long-term future for the housing industry, and especially for home sales in Master-Planned Communities, for which there is more underlying demand than supply, looks very positive.

The ranking of Mid-Year 2022’s 50 top-selling communities is based on total net new home sales as reported by each individual community. Preliminary sales numbers were provided by communities in mid-June and pro-rated in order to arrive at estimated mid-year sales, with final sales figures provided during the first weeks of July, and in some cases being updated periodically throughout the month. To be included in our ranking, MPCs must have a number of features. True MPCs are developed from a comprehensive plan by a master developer, and incorporate a variety of housing types, sizes, and prices, with shared common space, amenities, and a vital public realm. The best examples of MPCs are developed with a strong vision and comprehensive plan that guide development and unify the community through distinctive signage, wayfinding, entry features, landscaping, and architectural/design standards. Beyond the built environment, MPCs differentiate themselves from typical suburban subdivisions in that they provide a means for interaction among neighbors in the sense of the word “community.” They foster an environment within which generations can live better in terms of housing and the community environment, and many offer educational opportunities, neighborhood shopping and services, and even employment centers to complement the residential neighborhoods. Although rooted in a vision, the most resilient MPCs have flexible master plans that are environmentally sensitive, market responsive, and nurture the lifestyles of their residents.

Given the above criteria, we do not include the collective sales of multiple, separate communities that are unified only through marketing efforts rather than a preconceived community vision, nor do we include communities that are a collection of subdivisions that have few unifying elements other than consistent signage and name.

Article and research prepared by Gregg Logan, Managing Director, and Karl Pischke, Principal. Additional research support was provided by Shanren Brienan, Jameson Logan, and Blair Wheeler.

RCLCO provides real estate economics and market research services, strategic planning, and management consulting to real estate developers, investors, financial institutions, home builders, public agencies, and anchor institutions. Client’s turn to us for trusted, unbiased third party recommendations regarding highest and best use, product definition, market positioning/pricing, and absorption potential for any proposed development concept, site, or product type. Interested in learning more about RCLCO’s Master-Planned Community Services? Please visit us at www.rclco.com/master-planned-communities-services/.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.