January 7, 2025

In Summary

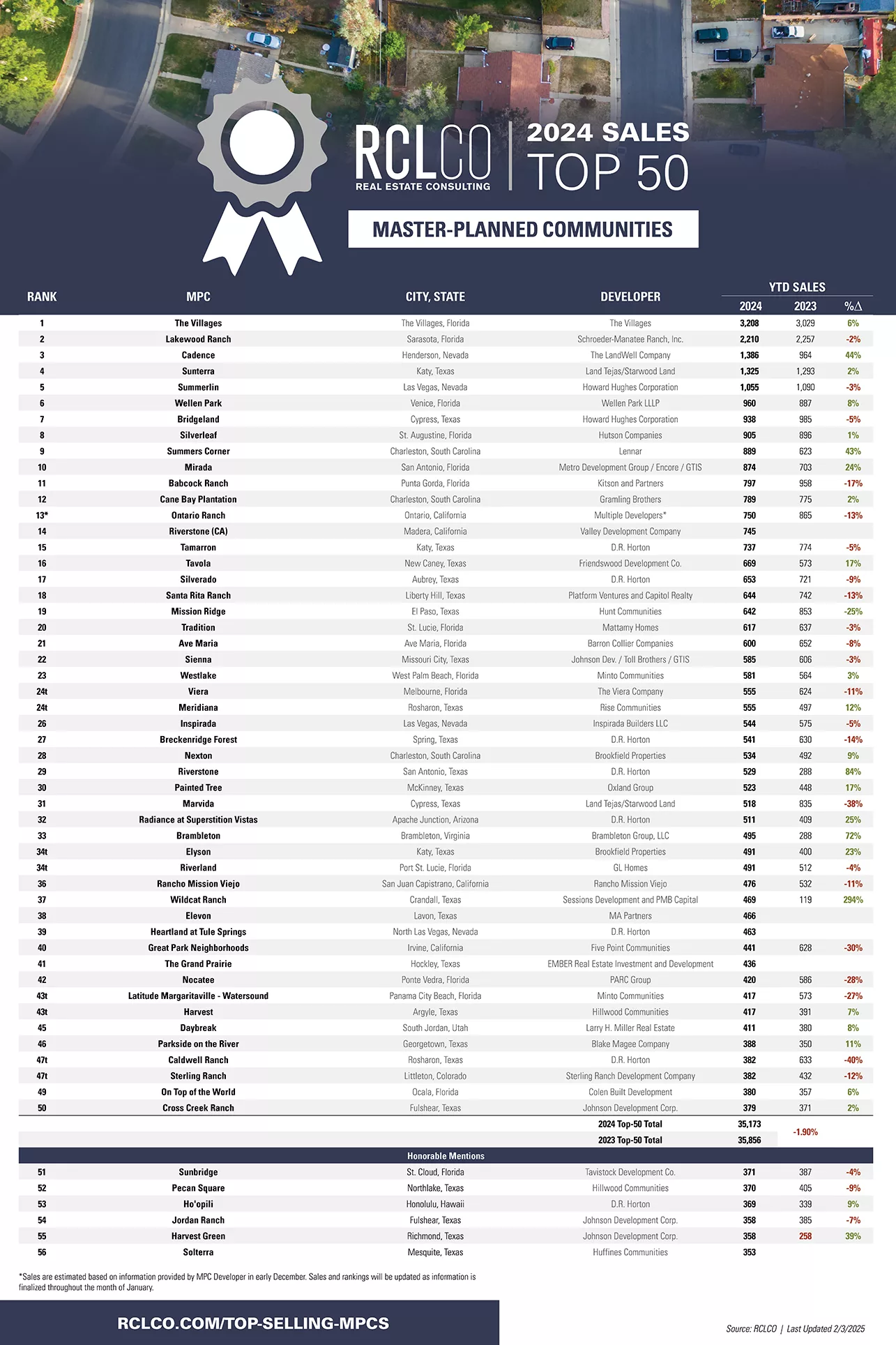

- New home sales among the 50 Top-Selling Master-Planned Communities were 2% below the pace set by top communities in 2023, a sign of resilient demand despite headwinds that included election uncertainty, hurricane impacts, “sticky” mortgage rates and continued affordability challenges.

- Limited resale inventory and the “lock-in” effect caused by elevated mortgage rates continue to make new homes an attractive option for consumers, particularly with builders willing to offer incentives.

- The Villages active adult community is once again the top-selling community in the nation with 3,208 sales, including sales in the new all-ages Middleton neighborhood

- Sarasota, Florida’s Lakewood Ranch claimed the number two spot overall with 2,210 sales. Cadence in Henderson, Nevada earned the third-place rank with 1,386 sales in 2024, a 44% increase over 2023.

- The Houston MSA was once again the top-performing metropolitan area with 12 communities in the Top 50, representing over 7,500 sales, or 22% of all sales among ranked MPCs.

- The state of Florida represented 38% of sales among ranked communities, followed by Texas at 35%.

- While mortgage rates have remained higher for longer than anticipated, RCLCO expects gradually declining rates will raise 2025 home sales moderately above the 2024 pace, assuming continued low unemployment, rising wages, and builder incentives.

Every year since 1994, RCLCO has conducted a national survey identifying top-selling master-planned communities (MPCs) through a rigorous search of high-performing communities in each state. This initiative, now in its 31st consecutive year, exists not only to recognize the most successful communities in the country, but also as a tool for monitoring the overall health of the for-sale housing industry, and a means of highlighting the trends affecting communities large and small. This process also serves as a mechanism through which to learn development best practices and pass along lessons gleaned from the MPCs that have pioneered their way into the top ranks. That information contributes to the knowledge base utilized in RCLCO’s MPC consulting practice. In the following report, RCLCO has surveyed MPCs throughout the country to update the rankings of The Top-Selling Master-Planned Communities of Mid-Year 2024.

The chart above summarizes RCLCO’s list of the 50 top-selling communities of 2024, including a comparison with their home sales in 2023 where applicable. Sales among the Top 50 communities were just 2% below the pace set by 2023 top-sellers. Considering the challenges seen throughout the year – from election uncertainty to severe weather events, as well as continued affordability concerns and “sticky” mortgage rates – this relative consistency among top-sellers highlights the resiliency of homebuyer demand and the perceived advantage of new homes in general and master-planned communities specifically.

The Villages community in Central Florida is once again the top-selling community in the country with 3,208 sales. Known as the largest active adult community in the country, The Villages now includes Middleton – a neighborhood designed for all ages. Sarasota, Florida’s Lakewood Ranch claims the 2nd place spot in this year’s ranks, with 2,210 sales – a strong performance which included a significant rebound following the impacts of Hurricane Milton in October, and election uncertainty through early November. Cadence, a LandWell Company community in Henderson, Nevada, earned the third-place rank with 1,386 sales, a 44% increase over 2023. The Houston MSA was once again the stand-out metropolitan area with 12 communities ranked within the Top 50, including 4th ranked Sunterra by Land Tejas and Starwood Land. The Houston Metro Area contributed to over 7,500 sales among the Top 50 MPCs, representing 22% of all sales among ranked communities.

Top-Selling Master-Planned Communities of 2024

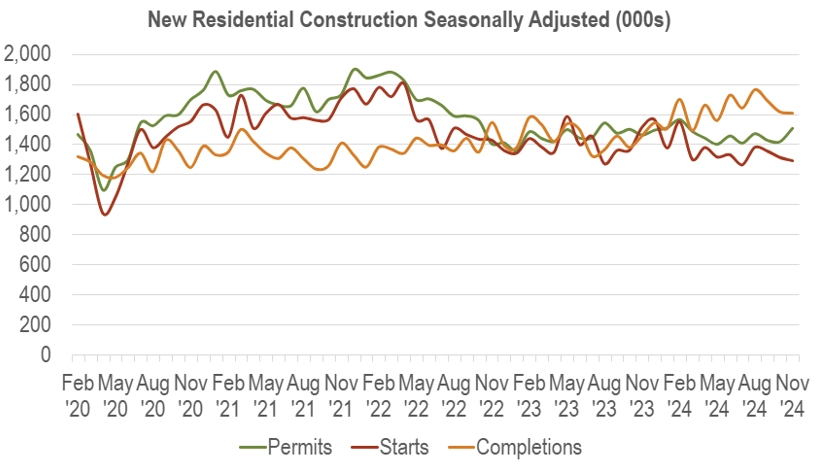

In our Mid-Year 2024 Update of RCLCO’s Top-Selling Master-Planned Communities Report, we reported that sales among Top-Selling communities had slightly outpaced the broader new home market but remained largely similar to the pace set by top MPCs in 2023. Given the headwinds associated with election uncertainty, hurricane and severe weather impacts, and continued affordability concerns due in part to higher for longer than anticipated mortgage rates, this relative consistency among 2024 top-performers highlights the resilient nature of U.S. homebuyer demand and the appeal of master-planned communities specifically. It is also encouraging that recent data suggests an uptick in both builder optimism and permitting activity following the conclusion of the 2024 presidential election (and the end of hurricane season).

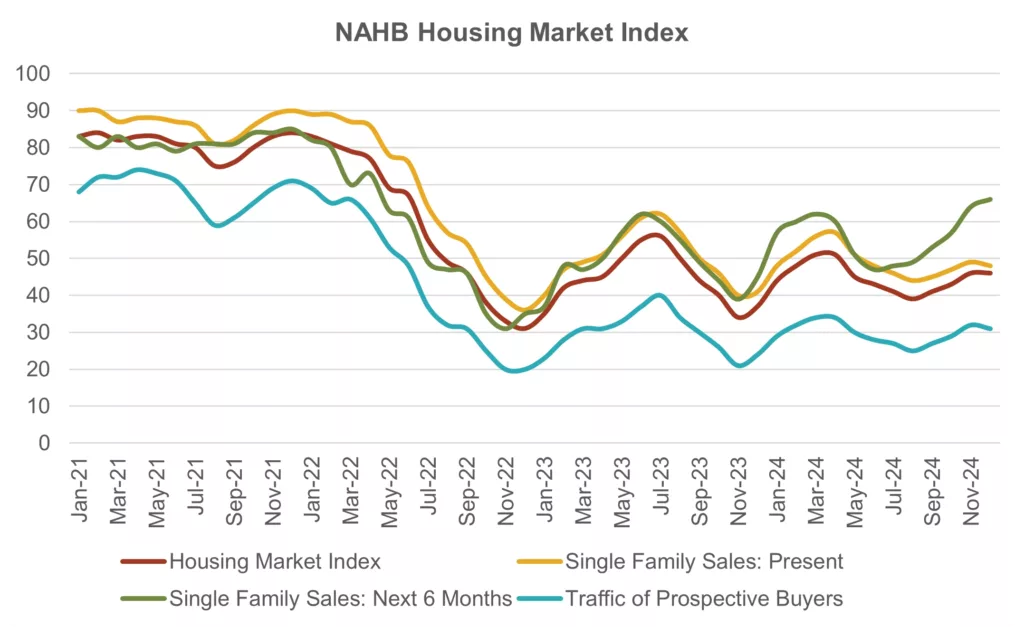

According to the U.S. Census Bureau, November 2024 saw a 6% month-over-month increase in building permits. Homebuilder sentiment, as measured by the National Association of Homebuilders (NAHB) Housing Market Index, has trended up to a score of 46 following an annual low of 39 just four months ago, in August 2024. According to the index, a score lower than 50 is an indication that a majority of builders lack confidence about the current and near-term outlook for housing. However, positive upward momentum coupled with significantly higher expectations for single-family sales over the next 6 months is encouraging for builders and master-planned community developers in 2025.

As we enter the new year, the U.S. economy shows substantial promise, with an unemployment rate at 4.2% and inflation easing to 2.5%. While not yet at the Federal Reserve’s target of 2%, inflation trended downward for most of 2024 (the Consumer Price Index for all urban consumers rose 2.7% over the last 12 months but was up 3.3% over the year in November). These economic conditions, combined with moderating interest rates and steady consumer demand, provide a good foundation for new home sales to improve throughout 2025, with continued strength projected into 2026. That said, certain factors could temper our enthusiasm, including the slightly elevated November 2024 CPI.

The Federal Reserve reduced the Fed Fund rate by another quarter point in December 2024, but mortgage rates have remained stubbornly high, hovering above 6%. As mortgage rates stabilize over the course of 2025 towards the low 6% range, we expect single-family home sales to outpace 2024 levels, particularly during the spring 2025 selling season.

Meanwhile, mortgage rates will remain higher than previously hoped, and Builders’ willingness to maintain incentives will continue to be essential to realizing stronger new home sales in 2025. Of course, the strength of the labor market also remains a critical factor driving housing demand. Low unemployment and rising wages have bolstered consumer confidence, sustaining new home demand despite elevated mortgage rates. While affordability remains a challenge, slower home price growth has offered some relief, and we expect that trend to continue in 2025.

The new administration’s policy landscape introduces both opportunities and risks. Deregulation and potential tax cuts could stimulate economic activity, benefiting housing markets. However, proposed tariffs, stricter immigration policies, and trade restrictions in general present potential downsides.

The U.S. economy begins 2025 on solid footing, providing a favorable backdrop for housing market growth. While uncertainty surrounding policy impacts remains a wild card, the resilience of the labor market, coupled with builders’ proactive strategies, positions the industry for a positive trajectory. Moving forward, master-planned communities that can maintain a focus on adaptability and responsiveness, particularly as it relates to pricing strategies and housing innovation, will be those that thrive in the evolving economic environment of 2025.

RCLCO has produced the Top-Selling Master-Planned Community Report since 1994, making it the longest-running publication on master-planned community performance in the industry. The ranking of communities is based on total new home contracts, net of cancellations, as reported by each individual community. Preliminary sales numbers are typically provided by communities in early December, with final sales figures provided during the first week of January. In some cases, sales figures are updated periodically throughout the month of January as communities finalize their records.

To be included in RCLCO’s ranking, MPCs must have several key features. True MPCs are developed from a comprehensive plan by a master developer, and incorporate a variety of housing types, sizes, and prices, with shared common space, amenities, and a vital public realm. The best examples of MPCs are developed with a strong vision and comprehensive plan that guide development and unify the community through distinctive signage, wayfinding, entry features, landscaping, and architectural/design standards. MPCs differentiate themselves from typical suburban subdivisions in terms of scale, as well as in how they provide a means for interaction among neighbors in the sense of the word “community.” They foster an environment within which generations can live better in terms of housing and the community environment, and many MPCs also offer educational opportunities, neighborhood shopping and services, and even employment centers to complement the residential neighborhoods. Although rooted in a vision, the most resilient MPCs have flexible master plans that are environmentally sensitive, market responsive, and nurture the lifestyles of their residents.

Given the above criteria, we do not include the collective sales of multiple, separate communities that are unified only through marketing efforts rather than a preconceived community vision, nor do we include communities that are a collection of subdivisions that have few unifying elements other than name.

More on the Top-Selling Master-Planned Communities

Article and research prepared by Karl Pischke, Principal, and Gregg Logan, Managing Director. Additional research support was provided by Kimberly Asbell, Christopher Bitter, Shanren Brienen, Maggie Henderson, and Jameson Logan.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.