March 19, 2024

Originally published via PREA

The US apartment sector is currently experiencing a rough patch in terms of elevated supply, reduced debt availability, higher borrowing costs, and lower values resulting from stagnant rents and higher interest rates. Some owners, particularly entities that used high leverage, are struggling to increase income and refinance maturing debt. However, mid- and long-term prospects continue to be positive because the US faces a chronic shortage of affordable housing.

Institutional investors have made large and increasing investments into the apartment sector over the past decade and now face difficult decisions about whether to sell or hold those positions. Those decisions are particularly challenging for development projects that have delivered or will deliver into operating and capital markets that are significantly less accommodating than when the projects were conceived.

Apartment Supply and Expected Fundamentals

Apartment vacancy rates hit cyclical lows in 2021 because of COVID-19-related demand and household moves. Taking advantage of low interest rates, developers responded with robust supply that peaked in 2023, elevating vacancy rates and bringing rent growth close to zero. Recent supply data indicate that the worst may be behind us:

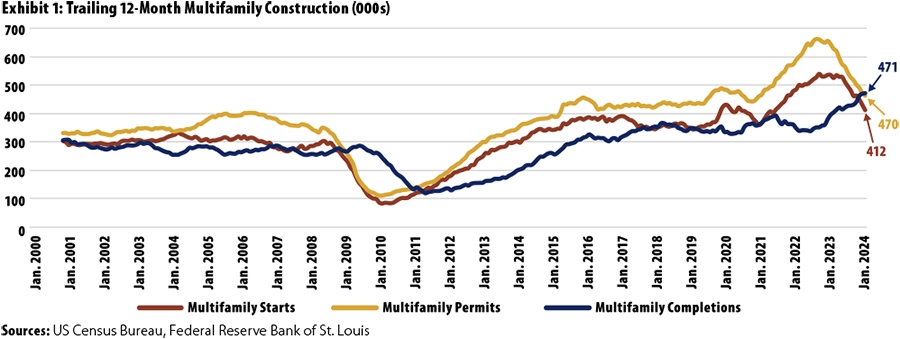

- New construction is slowing, although the pipeline of units under construction is still high. March 2024 apartment starts came in at an annualized rate of 290,000 units, compared with 515,000 units during the same month a year earlier. On a trailing-year basis, starts totaled 412,000 units, while completions were still high (and rising) at 471,000 units (Exhibit 1).

- As completions tail off in 2025, the apartment market is likely to move toward equilibrium (approximately 3% annual rent growth) in 2025 and 2026 (assuming moderate economic growth), particularly if homeownership remains out of reach for many.

- While new supply will not fall off entirely, headwinds to new supply include higher interest rates and exit cap rates, reduced and more expensive debt availability, and continued increases in operating costs (particularly insurance).

- Permits are also trending lower, totaling 1.7% of apartment stock for the 50 largest US apartment markets as of February 2024. However, new supply varies significantly by market: Austin, TX; Raleigh, NC; and Phoenix all had permit rates (as a % of stock) above 4.5% at that time.

Long-Term Drivers of Rental Housing

Although the US population growth rate has slowed over the past several decades, it is still positive and higher than in most developed countries. Moody’s forecasts that new household growth, including immigration, will average almost 1 million per year over the next ten years. In addition, the US has a housing shortage estimated at as much as 4 million units. Some of the other factors driving rental housing demand include these:

- The share of single households is increasing. Single households tend to rent rather than own.

- Income disparity is increasing, creating more renter households.

- Over the next five to ten years, the largest growth cohorts will be millennials (ages 35 to 50) and baby boomers (ages 65 and up). Both groups are more likely to own than rent, but that propensity could decline somewhat because of high homeownership costs and more rental options, such as single-family rental.

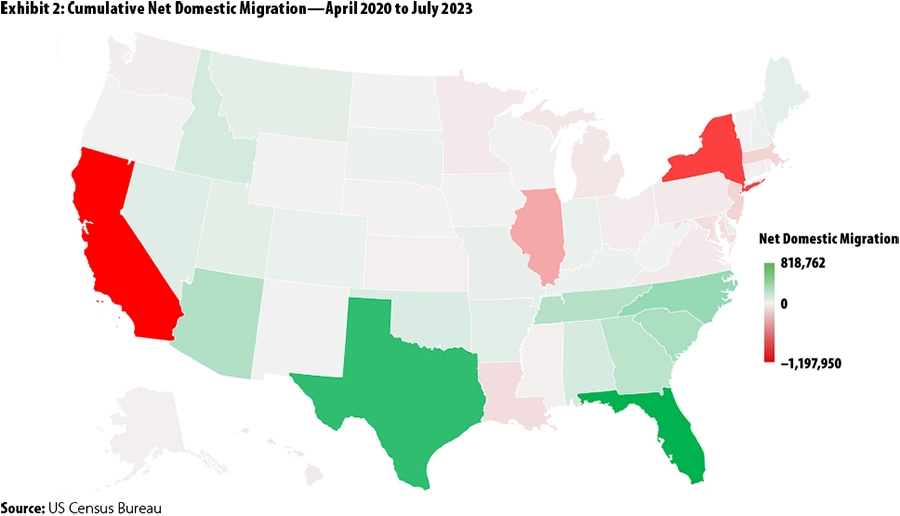

- There has been big movement from high-cost states (e.g., New York and California) to low-cost states, such as Texas and Florida (Exhibit 2). This trend will likely continue for the foreseeable future. Many of these domestic migrants will rent before deciding if and where to buy.

What Is the Optimal Hold Period?

As apartment investors contemplate a potentially improving leasing market in the midterm, they continue to struggle with both current and future values, particularly because interest rates remain elevated and volatile. This is causing many investors, whether they want to or not, to reevaluate their hold periods, for both existing and new investments. They also need to consider original investment intentions. Stabilized core investments are purchased primarily for long-term income and appreciation. Properties that are performing close to plan with little change to their competitive environments are likely to remain as core holdings. However, value-added and new construction can be carried in two different buckets—minimal hold period to maximize profits (either internal rate of return [IRR] or equity multiple) and renovation/build to core with the intention of holding for the long term.

- All else being equal, a shorter hold period should generate a higher IRR because of the time value of money and the erosion of returns over time. Conversely, a longer hold period should generate a higher return multiple as a result of both additional cash flow and the expectation of a higher exit value.

- All else is rarely equal, and a shorter time period reduces the window to execute a business plan. Additionally, even if there are no issues with business plan execution, the short time period increases (capital) market risk. Investors should seek adequate compensation for both these increased risks inherent in shorter-term investments.

- Longer-held assets are similarly subject to (capital) market risk, not only at the time of the underwritten exit but also during a refinancing, which will likely be necessary during the hold period. The impacts of these risks may be moderated by the positive impacts of growth and/or recovery cycle stages that will also likely occur during a longer-term hold.

- One risk that is significantly greater during a longer-hold period is the impact of an aging asset. Capital needs will increase over time, as will competition from new deliveries. Either or both of these conditions may necessitate costly property improvements to maintain competitiveness and value.

Impact of Leverage on Returns Over Different Hold Periods

As investors decide to hold their assets longer while awaiting improved market fundamentals, they are also reconsidering their leverage options, both today and for future investments. While leverage per se does not impact risk-adjusted returns, it is often an important part of both renovation and development business plans because expected higher-than-core returns can be amplified by leverage.

- Leverage can be a significant aspect of the (capital) market risk noted earlier. Should values decline and/or interest rates increase—both occurring currently—generating sufficient proceeds to repay short-term debt, particularly in higher-leverage scenarios, may be difficult. A longer hold period may allow for continued net operating income (NOI) growth that offsets the negative impacts of higher interest rates and/or lower valuations at exit.

- A longer hold period and the willingness to patiently achieve NOI growth may also allow an investment to achieve positive leverage that might not be possible during a shorter hold period.

That being said, the positive impacts of long-term growth may be eroded by loan amortization, which is more likely with longer-term debt.

Conclusion

Institutions and other entities invested in multifamily properties have to weigh challenging current operating and capital market conditions, as well as potential but uncertain improvements in those markets over the next several years as they plan for future sales and/or refinancings. Selling apartments today may make sense for portfolio reasons (either to rebalance or to invest in better risk-adjusted opportunities). Also, expiring loans may push some owners to sell rather than contribute more equity. However, given that both operating fundamentals and capital markets could improve over the next three to five years, investors may want to consider longer hold periods than originally planned.

Disclaimer: This article has been prepared solely for informational purposes and is not to be construed as investment advice or an offer or a solicitation for the purchase or sale of any financial instrument, property, or investment. It is not intended to provide, and should not be relied on for, tax, legal, or accounting advice. The information contained herein reflects the views of the author(s) at the time the article was prepared and will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing or changes occurring after the date the article was prepared.