August 9, 2023

Originally published in PREA Quarterly Magazine

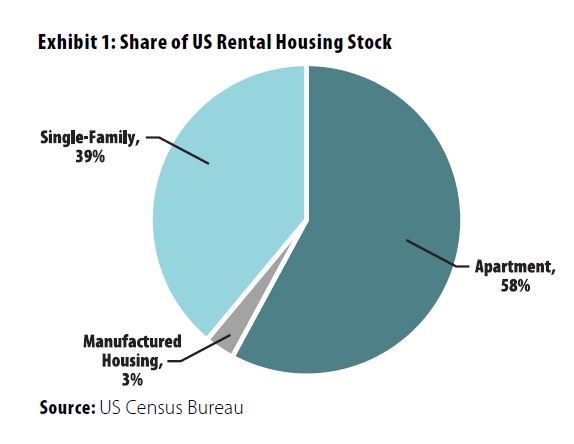

Single-family homes have been an important part of the US rental housing market for decades and even centuries. Individual investors have long owned houses they rent to a wide variety of tenants, including families, unrelated groups, and renters by choice. Single-family rentals (SFRs) make up about 39% of the overall US rental housing inventory, with multifamily apartments composing 58% and manufactured housing accounting for 3% (Exhibit 1). The majority of SFR stock is more than 40 years old, with relatively little constructed over the past ten years.

Institutional investment in the SFR sector was very limited until after the global financial crisis, when US opportunity funds and other investors started to purchase deeply discounted houses to rent out. Because the houses were scattered across metro areas, there were concerns that managing houses that were both spread out and nonstandard in terms of appliances, layouts, and level of repair would be inefficient.

Institutional investment in the SFR sector was very limited until after the global financial crisis, when US opportunity funds and other investors started to purchase deeply discounted houses to rent out. Because the houses were scattered across metro areas, there were concerns that managing houses that were both spread out and nonstandard in terms of appliances, layouts, and level of repair would be inefficient.

Early investors in SFRs proved the doubters wrong and were able to efficiently purchase, lease, operate, and maintain widely disparate SFR portfolios, developing new technologies and systems along the way. Several early investors utilized the public markets as an exit strategy, with the two SFR REITs—American Homes 4 Rent and Invitation Homes—having a combined market cap of more than $36 billion, as of July 1, 2022.

Types of SFRs

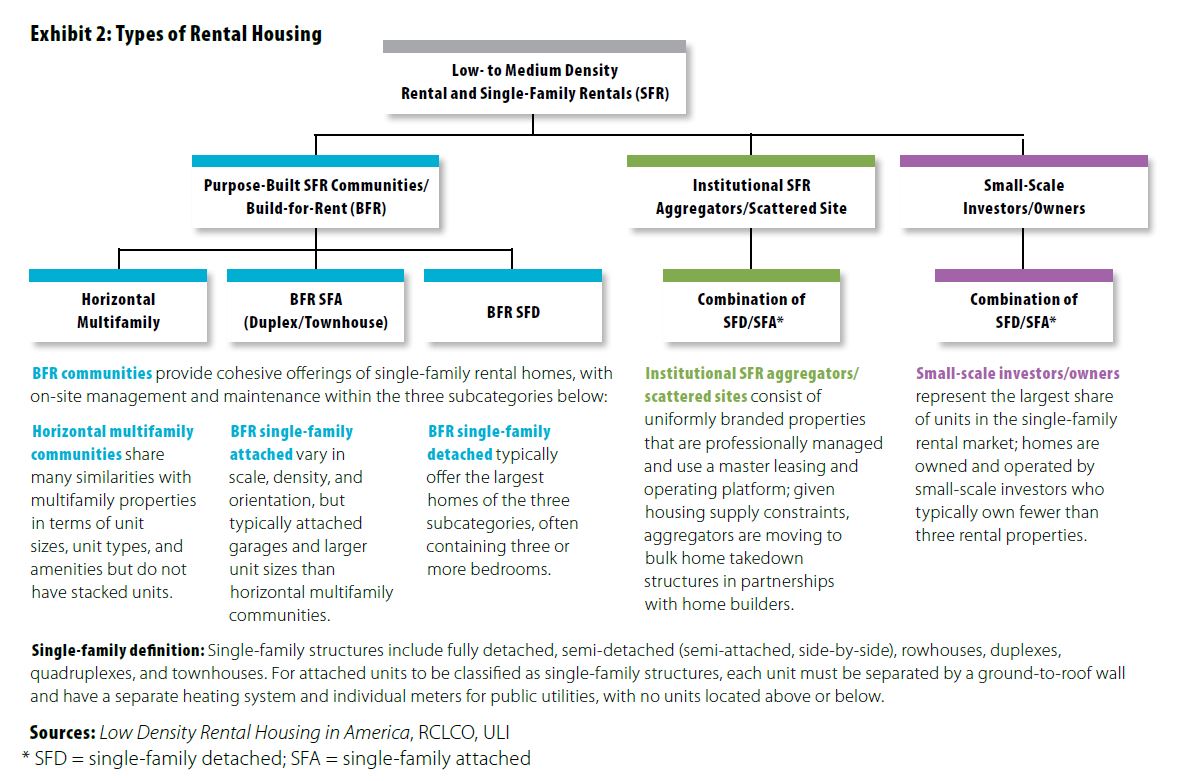

The institutional SFR sector initially developed using a scattered-site approach—most properties were purchased on a one-off basis based on availability rather than a geographic strategy. Properties were acquired in a variety of ways: on the open market, through foreclosures, and in bulk sales. Many of the early investments were in the metro areas most affected by the financial crisis–related housing bust, including Phoenix, Atlanta, and Riverside, although there was and is investment activity in many other markets. Over the past three to five years, home prices have risen across most of the US, making individual house investments more difficult and less attractive financially. Although SFR companies use the scattered-site approach, they and other market participants have started to shift to purpose-built SFRs.

Purpose-built SFRs are generally referred to as build-to-rent (BTR) or build-for-rent (BFR) communities. The appeal of BTR is control over design, materials, HVAC equipment, etc., that should lead to lower operating and maintenance costs over the long run. In addition, a single location should result in lower leasing and management costs. Finally, many BTR communities are large enough to support amenities (e.g., pool, clubhouse) to better compete with both SFR and traditional apartments. Because the BTR model is relatively new, performance data are scarce, but early indications are that tenant demand is very strong.

BTR styles include detached houses as well as attached townhouse-style homes. Most but not all have garages, off-street parking, and private outdoor space; so-called “horizontal apartments” may provide only open parking. BTR communities generally provide more amenities than scattered-site SFRs do and more space and privacy than traditional apartments offer (Exhibit 2).

Performance

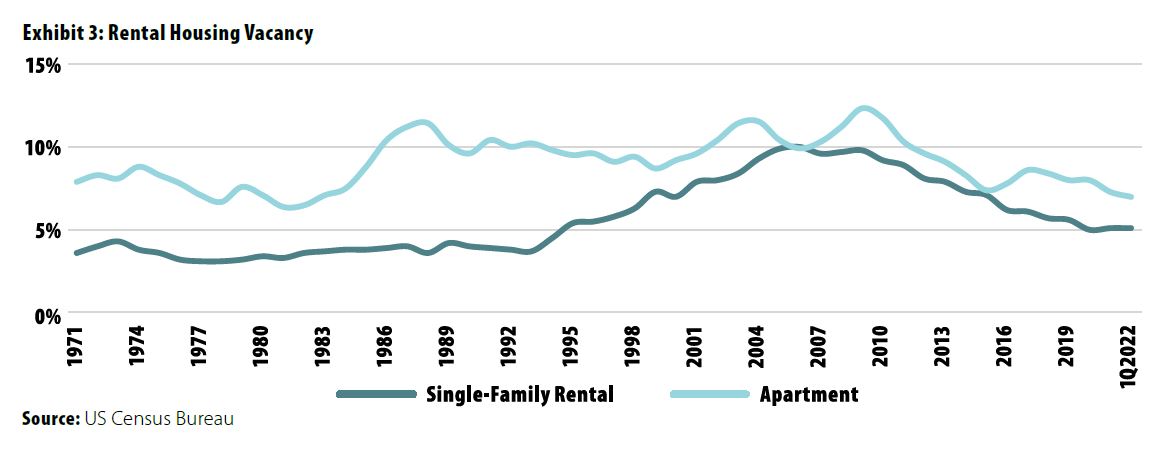

All signs point to strong operating and financial performance by SFRs, both absolutely and relative to apartments. SFR vacancy rates have been below apartment rates for decades, as shown in Exhibit 3. Operators point to an overall shortage of SFRs as well as much less turnover as drivers of lower vacancy rates. SFRs also have exhibited strong and stable rent growth, with a long-term average consistent with multifamily rent growth. SFRs have been much more resilient than apartments to economic shocks, with rents growing consistently throughout the dot-com crash, the global financial crisis, and the COVID-19 pandemic, in contrast to apartment rents, which contracted in response to each crisis.

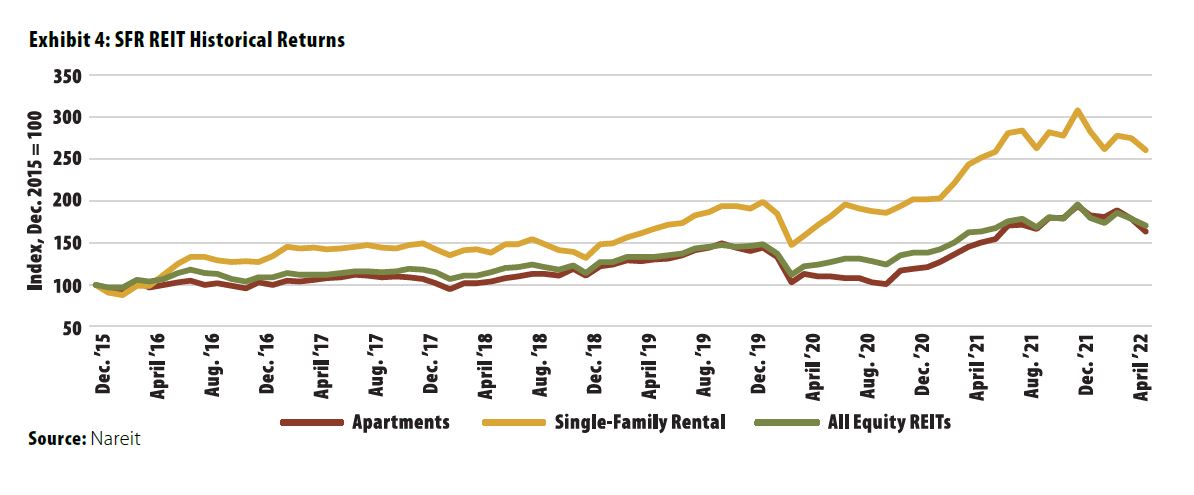

Data on financial performance by institutional investors is not readily available, but the track record of the two SFR companies trading as publicly listed REITs points to strong performance. Although down in 2022, SFR REITs have generated 160% returns since Dec. 2015, compared to 70% for both apartment REITs and all-equity REITs (Exhibit 4). The SFR REITs reported that same-home turnover declined from 33% in 2016 to 25% in 2021, well below multifamily levels. In addition, net operating income margins have stayed relatively consistent in recent years at approximately 65%–70%, comparable to multifamily levels.

Opportunities

Given that the SFR sector of rental housing has proved to be a viable business model, institutional investors have many compelling reasons to consider investing in the sector:

- Strong and Resilient Demand Drivers: Shifts in demographics, increased familiarity with the product type, changing housing preferences, and elevated for-sale costs have led to strong and rising demand. SFRs appeal to a wide range of tenants: young families, empty nesters, temporary residents, etc. Additionally, the COVID-19 downturn has proved SFRs to be a cyclically resilient asset.

- Limited New Supply: Although BTR development is increasing, it is not keeping up with demand. In addition, some SFRs are being sold to owner-occupiers because of rising home prices.

- Efficiency in Operations: Operating margins are consistent with the multifamily sector.

- Attractive Economics: SFRs show strong rent and revenue growth and low vacancy and turnover rates.

- Large, Fragmented, and Dislocated Market: Institutional investors that can achieve scale have a competitive advantage relative to the “mom and pop” owners that currently dominate the sector.

The demand for SFRs is particularly compelling and likely to stay that way. The millennial cohort has reached the life stage at which many prefer single-family housing over apartments. At the same time, their ability to purchase a home is restrained because home prices have steadily risen over the past decade, and many millennial households have high debt levels and insufficient savings for down payments. SFRs also appeal to empty nesters, retirees, and temporary residents. Finally, the recent shift toward remote work has lessened the importance of employment location in housing choices, reducing the cost and friction of suburban locations.

Challenges

There are inherent risks in the SFR sector given its very limited history as an institutional property type:

- Social and Political Concerns: Housing affordability concerns present social and regulatory risks.

- Rising Home Prices: As home prices rise, the economics of SFRs become less attractive.

- Increased Competition: More and more investors (institutional and private) are allocating capital to the sector, leading to higher prices and lower returns. At least $45 billion was committed to SFR strategies in 2021, according to the Wall Street Journal.

- Economic and Capital Market Uncertainty: The US economy has clearly slowed, and a recession may be forthcoming. In addition, borrowing costs have risen sharply following the Federal Reserve’s increases in the funds rate.

There are additional challenges and concerns for the BTR strategy:

- Rising Home Prices: As home prices continue to rise, BTR developers/investors will increasingly compete with home builders for lots/land.

- Development Dynamics: Rising costs of land, labor, and material as well as uncertainty over future operating and capital expenditures and entitlements are concerns.

- Newness of Product Type: The sector has a limited number of BTR communities despite the recent momentum. As such, there is still uncertainty about what product types work best where, and limited developers/operators with robust track records are in the sector.

Of the various challenges, social and political concerns, particularly the impact on home ownership, are getting the most attention currently. Redfin reported that “investors bought 18.4% of the US homes that were purchased in the fourth quarter, a record high.” The Wall Street Journal reported that this is reducing supply, particularly for first-time buyers, and driving up costs. Even though institutions own only 3% to 4% of SFRs, said the Journal, that number will continue to grow as already-committed capital is deployed. Other concerns include substandard maintenance and predatory rent increases when tenants have limited options.

BTR communities face fewer concerns because developers provide new houses that arguably add affordable housing to the overall housing supply. Opponents argue that BTR houses are reducing the supply of affordable starter homes, although it is not clear that developers would build starter homes in the absence of BTR homes. Sales of new homes priced under $200,000 went from 43% of total units in 2009 to 2% in 2021. The BTR industry accounted for less than 4% of all housing starts in 2021.

Summary

The institutional SFR sector has generated very strong returns since its inception in the early 2010s. It provides a product—detached homes for rent—that is in high demand, with limited new supply on the horizon. Institutional interest in the SFR sector will likely continue to increase, given strong fundamentals and compelling and likely stable returns.

Although purchasing scattered-site existing units is still possible, developers have found that rising prices make the strategy less compelling. In addition, critics argue that buyers of existing units price some first-time buyers out of the market. There is talk of greater regulation of that segment of the market, including purchasing restrictions and rent control.

The BTR strategy is gaining share because building rental housing is often less expensive than purchasing it. The BTR approach also provides built-in efficiencies because all units are at a single location with common components. Although there is less pushback about its impact on the for-sale housing market, some opposition to the strategy remains. The market is still relatively small—only eight owner/operators currently have more than ten BTR communities across the US. Sponsors will likely have to do a better job of addressing concerns of local communities and housing advocates, but the overall demand/supply story is very compelling for long-term investors.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.