June 27th, 2024

The events of the last several years have generated unprecedented volatility in the RCLCO Real Estate Market Index (RMI) – with significant swings in sentiment (both positive and negative) resulting from COVID-19, inflation, and rising interest rates. For the first time since mid-2021, the RCLCO sentiment index is showing positive signs that point to a recovery in the real estate market. We also asked our survey participants to weigh in on the upcoming U.S. Presidential election, and the impact that it could have on our industry.

Key Takeaways

- The RCLCO Current Real Estate Market Sentiment Index (RMI)[1], has improved markedly over the past six months, ending close to 40 in the most recent survey, an increase of 2.5x from year end. The index is now hovering right at the threshold of recovery – an RMI less than 40 is typically consistent with a period of real estate market distress/recession.

- On an even more positive note, a large share of respondents predict that real estate market will continue to improve over the next 6-12 months – the Future RMI is predicted to increase to over 55 over the next 12 months, indicating a return to recovery and expansion within the next year.

- Consistent with this expected recovery in real estate, fewer respondents believe the U.S. is at risk of slipping into a recession anytime soon – in fact nearly 60% believe that a recession is unlikely to occur in the next 24 months or is more than a year away. In contrast, a year ago 76% of respondents thought that the U.S. economy either was already in a recession or that one was imminent within the next 6-12 months.

- More than half of respondents (55%) predict that Trump will win the upcoming U.S. presidential election, compared with 43% who predict Biden and 2% third party. For context, the most recent national poll averages (as of June 25, 2024) show Biden and Trump even at 41% with Kennedy polling at just over 9%.

- Of those who predict Trump will win, 65% believe this will have a positive impact on the real estate industry. For respondents who believe Biden will prevail, only 24% believe this will a positive impact on the real estate industry and 59% anticipate the impact to be neutral.

- The biggest challenges facing real estate companies include availability and cost of capital (53%) followed by construction costs (44%), labor availability and/or cost (36%), and inflation/G&A costs (32%).

- Looking towards the next 12 months, survey respondents expect most real estate sectors to be in some stage of recovery, although some niche sectors – such as self-storage, grocery/necessity retail, and industrial – are anticipated to continue to show resilience after avoiding downturn conditions this cycle.

- The sentiment around inflation seems as stubborn as inflation itself – 39% believe inflation will continue to decrease, 35% believe it will remain the same, but thankfully only 25% anticipate that rates will rise.

Respondents expect conditions to improve…

The RMI index has had a series of dramatic peaks and valleys during the past several years. After an initial robust recovery in 2021, sentiment dropped again in 2022-2023 and appears to be in the early stages of a more gradual recovery in 2024. With inflation slowing, the market is anticipating potential future rate cuts which has fueled optimism in the real estate sector. The current RMI increased to 38.9 as respondents see conditions improving, and the future expectation of 55.5 would bring the market out of recessionary territory.

RCLCO National Real Estate Market Index

Source: RCLCO

The current index at 38.9 puts the market right at 40, a threshold between a healthy market and a period of economic distress or recession. Looking forward, respondents predict that the sentiment index will increase by nearly 17 points over the next 12 months to 55.5, out of the distress/recession zone.

How Would You Rate National Real Estate Market Conditions Today Compared with One Year Ago?

Source: RCLCO

Browse Past Sentiment Surveys

- 2024 Looking Better Than Before

- RCLCO Real Estate Sentiment Hit All Time Low as Recession Looms

- Real Estate Market Sentiment Dips into Recessionary Zone Amid Economic Uncertainty

- Despite a Slight Decline, Sentiment Regarding the Real Estate Market Remains Strong

- Explore ten years of results from all Sentiment Surveys

12-Month U.S. Real Estate Market Predictions over Time

Source: RCLCO

Market sentiment remained fairly negative in 2022 and 2023. In Mid-2024 respondents felt more optimistic with a growing share indicating conditions were likely to get moderately better over the next year.

- The outlook for the upcoming year predicts recovery, though opinions are still mixed. Mid-2024 marks an inflection point when a larger respondent share predict conditions will improve than get worse; the last time forward-looking sentiment was skewed favorably like this was in 2021.

U.S. Presidential Election

We asked survey respondents to predict the outcome of the 2024 U.S. Presidential election in November. Respondents predicted Trump would win the election over Biden with a 55% to 43% spread. The remainder of respondents selected a third-party candidate. Please note this data was collected in early June, prior to the June 27th debate.

U.S. Presidential Election Predicted Winner

Source: RCLCO

We then asked respondents how they felt their predicted winner would impact the real estate industry. The results show that respondents in the real estate industry overwhelmingly feel that Trump will have a positive impact on market conditions, while Biden’s impact is more mixed with the largest share believing the impact will be neutral.

Source: RCLCO

Recession in Retreat

Over half (62%) of respondents feel that a recession will occur at some point in the next two years, down from 71% at the 2023 year end survey. Only a quarter (26%) believe that this recession will occur within the next year. The share of respondents who believe a recession will occur is dropping, and of those who believe a recession will occur in the next two years, only 9% believe the severity will be greater than a -2% decrease in GDP. Only 42% believe that this recession is happening now or will occur within the next year. The share of respondents who believe a recession will occur is dropping, and of those who believe a recession will occur in the next two years, only 6% believe the severity will be greater than a 2% decline in GDP.

When Will the Next U.S. Recession Occur?

Source: RCLCO

What Do You Believe the Depth of Recession Will Be?

Source: RCLCO

Signs of Recovery

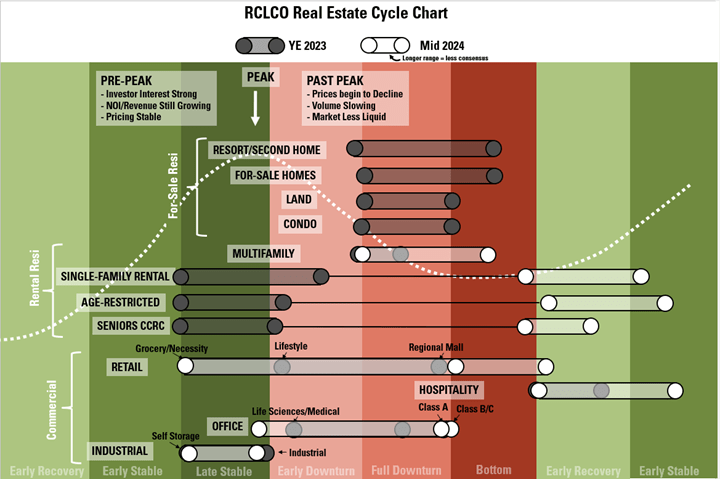

In Mid 2024, we are continuing to experience stress and corrections in the residential real estate sectors. As with our previous survey, we reflect the range of responses (when there is less consensus) in the chart below – the longer the bar, the larger the variation in responses. Commercial uses often have more variation since they contain more subsectors of varying performance than the residential groupings, and that detail is labeled on the chart. Sentiment around the for-sale residential sectors was mixed – with some signs of slight improvement after a lull that may signal a return to more typical market conditions after a period of inflated pricing and high sales volume. Multifamily rental has moved into downturn, though subsectors such as single-family rental, age restricted, or seniors housing may be emerging into early recovery. Industrial remains stable, and hospitality continues to emerge into recovery. Retail show more variation as grocery/necessity retail remains resilient, malls are in downturn, and lifestyle retail shows signs of recovery. Respondents indicated that all types of office are currently in downturn.

Cycle Stage Movement over Past Six Months

Many Land Uses Emerging from Downturn

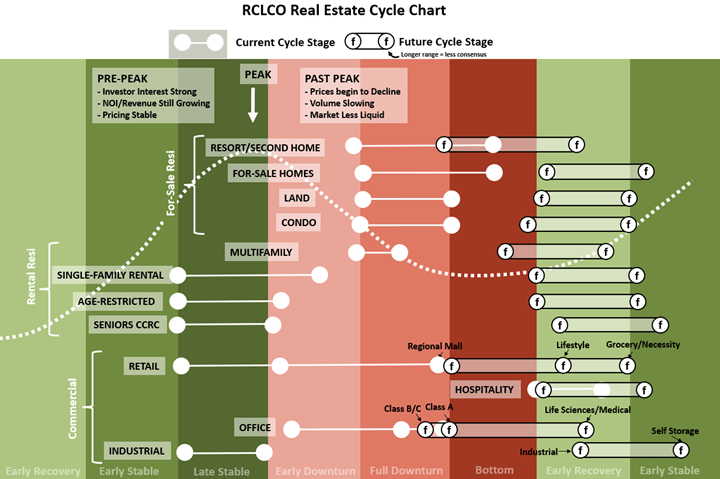

Looking forward, most of the residential sectors are predicted to move into recovery stages, with some of the for-sale sectors having the least certainty. The outlook for commercial sectors is also increasingly positive as hospitality, grocery-anchored retail, lifestyle retail, storage and data centers, and life sciences and medical office are expected to either remain stable or emerge into early recovery. Recovery in sectors such as traditional office and regional malls is expected to lag behind other sectors, remaining in downturn in the coming year.

Economic Indicator Predictions for the Next Year

Generally speaking, respondents expect key indicators that have an impact on real estate to improve, but at a modest pace/rate.

What Do You Expect to Happen with the Following Economic Indicators Over the Next 6 to 12 Months Nationally?

Source: RCLCO

- The majority (58%) of respondents said that interest rates will decrease at a moderate pace, and 34% predict that interest rates will remain the same. This shows a slight improvement since year end.

- End of year cap rate forecasts are mixed and follow those from Year End 2023. 28% predicted an increase, 28% predicted decrease, and 38% predicted them to stay the same.

- Inflation is predicted to either stay the same or decrease moderately as it has already reached a relatively low rate of 3.3% (not seasonally adjusted) as of May 2024, 37% believe that inflation will decrease moderately, 35% believe it will stay the same, and 23% feel it will increase moderately.

- Nearly half (47%) believe that capital flows to real estate will increase.

- Views on construction costs were somewhat pessimistic with 47% predicting an increase and 34% predicting no change.

- The homeownership rate was predicted to remain the same.

Because it has a big impact on real estate valuation and debt costs, where do you think the 10-year treasury will be 24 months from now?

Source: RCLCO

RCLCO POV

ECONOMIC OUTLOOK

The U.S. economy has held up better than expected in 2024, particularly the labor market; and while we believe that both will slow over the next year or so, we do not expect a recession as a base case. Stronger growth (>2%) is possible (~15% probability) if consumer spending stops slowing and possibly accelerates and companies taper currently anticipated layoffs. A shallow recession is also possible (~20% probability), with a government shutdown, further credit problems, higher oil prices, or an escalation of geopolitical conflict as possible triggers. The recent slowing of the job market should lead to slower wage growth in the near term. Combined with an eventual inflection in housing costs, the Consumer Price Index (CPI) should move close to 2% in 2025. Given these trends, we do not have any reason to disagree with the market consensus that the Federal Reserve will cut the Fed funds rate once in 2024 and at least three times in 2025. We predict all cuts to be 25 basis points which would take the target rate to 4.25-4.5% by year-end 2025, lower than today’s rates but still notably higher than in recent years.

REAL ESTATE SECTORS AND CAPITAL MARKETS

Overall, capital markets have not been supportive of real estate. As of the end of May, the yield on the 10 Year US Treasury Note was at 4.51%, up 63 bps year-to-date and 87 bps compared to a year ago. The yield has trended down so far in early June. We think that long rates will settle around 4%, but it might take a few years to get there.

Real estate fundamentals have generally softened in 2024 due to heightened supply, particularly for apartments and industrial, despite above average demand/absorption. Neighborhood and strip retail fundamentals have improved as new supply is minimal, while office has suffered from weak demand and continued new construction. We expect office rents to decline for the next several years, contributing to a continued wave of defaults and distressed sales. The life sciences office/lab sector has cooled with the overall office market, but we expect this sector will be among the first to recover. We expect industrial and apartment fundamentals to turn the corner with lower vacancies and better rent growth in 2025, with normal variation by market.

Niche or specialty sectors continue to be the bright spot in the real estate market. NCREIF has recognized the growing importance of these property types by adding many to the NCREIF Expanded NPI. Within the new NPI, data centers, manufactured housing, student housing and hotels have all posted positive total returns (compared to NPI of -6.9%) over the past year.

The real estate capital market is showing early signs of a recovery, with a spike in CMBS issuance in the first quarter. Average commercial mortgage rates are down slightly so far in 2024 despite higher base rates. Spreads have been well above average and will likely continue to fall over the next year.

NOT ALL MARKETS ARE CREATED EQUAL

Within the U.S., Sunbelt markets will continue to attract younger residents and employees driving strong real estate demand for years to come. Austin and Dallas stand out for high percentage and absolute growth, respectively. While supply responses may restrain rent growth in Sunbelt markets, opportunities for development/build to core will be attractive. The key 20-34 year age cohort is leaving more expensive coastal markets, notably New York, Los Angeles, and San Francisco. Weak office markets in Gateway cities will create ongoing problems with revenue and CBD vitality, although we believe that urban residential markets within diversified economies will continue to thrive. Despite unfavorable demographic trends, we call out New York and Los Angeles for their global dominance in finance and entertainment, respectively, attractiveness to foreigners, and their overall diversity, and we continue to recommend investments in those markets.

THE MOST IMPORTANT ELECTION OF OUR LIFETIME – AGAIN…?

The 2024 US presidential election has created heightened uncertainty, although past elections have not led to drastic changes in economic performance. The presidential winner will be crucial, but control of the House and Senate will dictate actual policy steps. Areas of potential differentiation are tax policy and government spending. On the other hand, both candidates seem to be supportive of maintaining or expanding import tariffs.

Who Took the Survey?

RCLCO’s Real Estate Market Sentiment Survey tracks the sentiments of a highly experienced pool of real estate professionals from across the country and the industry. A majority (72%) of respondents have worked in the real estate industry for 20 years or more, with an average respondent tenure of approximately 26 years, and 81% of respondents are C-suite or senior executives in their organizations.

Years of Experience in Real Estate

Source: RCLCO

Position in Organization

Source: RCLCO

Developers and builders comprise the largest share of respondents, at 40% of the sample. Another 20% are investors or capital allocators, followed by 5% in design or architecture firms. The remaining 35% of respondents come from a variety of other types of organizations within the real estate industry and public sector.

Type of Organization

Source: RCLCO

The respondent mix is representative of the U.S. as a whole: however, it is weighted towards those who report working primarily in coastal and Sunbelt markets. This respondent mix reflects markets where there has been significant development activity in this cycle.

Primary Region/Market

Source: RCLCO

Sentiment Survey article and research prepared by Charles Hewlett, Managing Director; and Kelly Mangold, Principal. RCLCO Point of View prepared by Charles Hewlett, Managing Director.

References

[1] The Real Estate Market Index (RMI) is based on a semiannual survey of real estate market participants and is designed to take the pulse of real estate market conditions from the perspective of real estate industry participants. The survey asks respondents to rate real estate market conditions at the present time compared with one year earlier (Current RMI), and expectations over the next 12 months (Future RMI). The RMI is a diffusion index calculated for each series by applying the formula “(Improving – Declining + 100)/2.” The indices are not seasonally adjusted. Based on this calculation, the RMI can range between 0 and 100. RMI values in the 60 to 70+ range are indicative of very good market conditions. Values below 30 are typically coincident with periods of economic and real estate market stress/recession.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Copyright ©️ 2024 RCLCO. All rights reserved. RCLCO and The Best Minds in Real Estate are trademarks of Robert Charles Lesser & Co. All other company and product names may be trademarks of the respective companies with which they are associated.