December 19th, 2024

The events of the last several years have generated unprecedented volatility in the RCLCO Real Estate Market Index (RMI) – with significant swings in sentiment (both positive and negative) resulting from COVID-19, inflation, and rising interest rates. For the first time since an initial short-lived recovery in 2021, the RCLCO sentiment index has moved solidly into recovery territory at year-end 2024. We also asked our survey participants their thoughts on how the recent presidential election results would impact the real estate industry.

Key Takeaways

- The RCLCO Current Real Estate Market Index (RMI) [1] has shown strong improvement over the past six months, ending at 65 in the most recent survey, an increase of over 25 points since mid-year. The index has now moved solidly into recovery territory – an RMI above 60 is typically indicative of positive or improving market conditions.

- The survey forecasts good times ahead, a large share of respondents predict that real estate market will continue to improve over the next 6-12 months – the Future RMI is predicted to increase to 82 over the next 12 months, indicating a return to expansion within the next year.

- Looking towards the next 12 months, survey respondents expect most real estate sectors to be in recovery or early stable phases. Some niche sectors – such as self-storage, grocery/necessity retail, and industrial – are anticipated to continue to show resilience after avoiding downturn conditions this cycle.

- Our mid-year survey respondents correctly predicted a Trump win. Over half (54%) believe that a Trump presidency and a Republican-controlled Congress will have a positive impact on the real estate industry, 21% believe the impact will be neutral, 17% believe it will be negative, and the remaining 8% are unsure.

- Climate risk has factored into over half (56%) of respondent’s real estate activities, in terms of geographic diversification, avoiding certain area, insurance costs, valuations, etc.

Respondents expect conditions to improve…

The RMI index has had a series of dramatic peaks and valleys during the past several years. After an initial robust, but short-lived, recovery in 2021, sentiment dropped again in 2022-2023 but has now moved solidly into a positive state at year-end 2024. With inflation stabilizing and rate cuts underway, respondents believe the real estate sector has a bright outlook for 2025. The current RMI increased to 64.8 as respondents see conditions improving, and the future expectation of 82.08 conveys the positive sentiment that the real estate sector has for the year to come. It is important to note that the survey results predated the Fed’s signal that it would likely only cut rates two times in 2024 vs. the previous four cuts.

RCLCO National Real Estate Market Index

Source: RCLCO

Detailed Results

Current market sentiment remained fairly negative in 2022 and 2023. In Mid-2024 respondents felt more optimistic with a growing share indicating conditions were getting moderately better, and at year-end more than half felt conditions were improving.

How Would You Rate National Real Estate Market Conditions Today Compared with One Year Ago?

Source: RCLCO

Browse Past Sentiment Surveys

- From Polling Places to Commercial Spaces: Does Real Estate Prefer Trump or Biden

- 2024 Looking Better Than Before

- RCLCO Real Estate Sentiment Hit All Time Low as Recession Looms

- Real Estate Market Sentiment Dips into Recessionary Zone Amid Economic Uncertainty

- Explore ten years of results from all Sentiment Surveys

The outlook for the upcoming year predicts expansion, with three-quarters (76%) of respondents believing conditions will continue to improve over the following year.

12-Month U.S. Real Estate Market Predictions over Time

Source: RCLCO

Trump Bump for Real Estate

At mid-year, 55% of respondents correctly predicted a Trump win for the 2024 U.S Presidential election. We asked survey respondents how they felt their predicted winner would impact the real estate industry. The results show that just over half (54.0%) believe that a Trump presidency with a Republican-controlled Congress will have a positive impact on the industry. A smaller share (21.2%) felt the impact would be neutral, and 17.2% felt the impact would be negative. Republican administrations typically favor less regulation, and this could benefit the real estate industry. However, talk of tariffs and tougher immigration enforcement could spark another inflationary spike, exacerbate an already difficult labor market, and lead the Fed to slow interest rate cuts, none of which will be helpful to the real estate sector. Please see more on this topic in our advisory on Trump’s second presidency.

What Impact will a Trump Presidency and a Republican-controlled Congress have on the Real Estate Industry?

Source: RCLCO

Climate Risk

With the high-profile climate disasters of the past year, we asked respondents how climate risk due to flooding, hurricanes, wildfires, and other natural disasters has factored into their real estate activities. Over half (56%) of respondents say this has factored into their activities – though only 12% say that this impact is significant. Notwithstanding the survey results, and despite receiving increased attention over the past several years, RCLCO has seen little evidence that climate change has had a material impact on real estate investment and development activity. However, this could change in response to increasing insurance costs in selected at risk markets and/or deals.

Has Consideration of Climate Risk Factored into Your Company’s Real Estate Activities in Terms of Geographic Diversification, Avoiding Certain Areas, Insurance Costs, Valuations, etc.?

Source: RCLCO

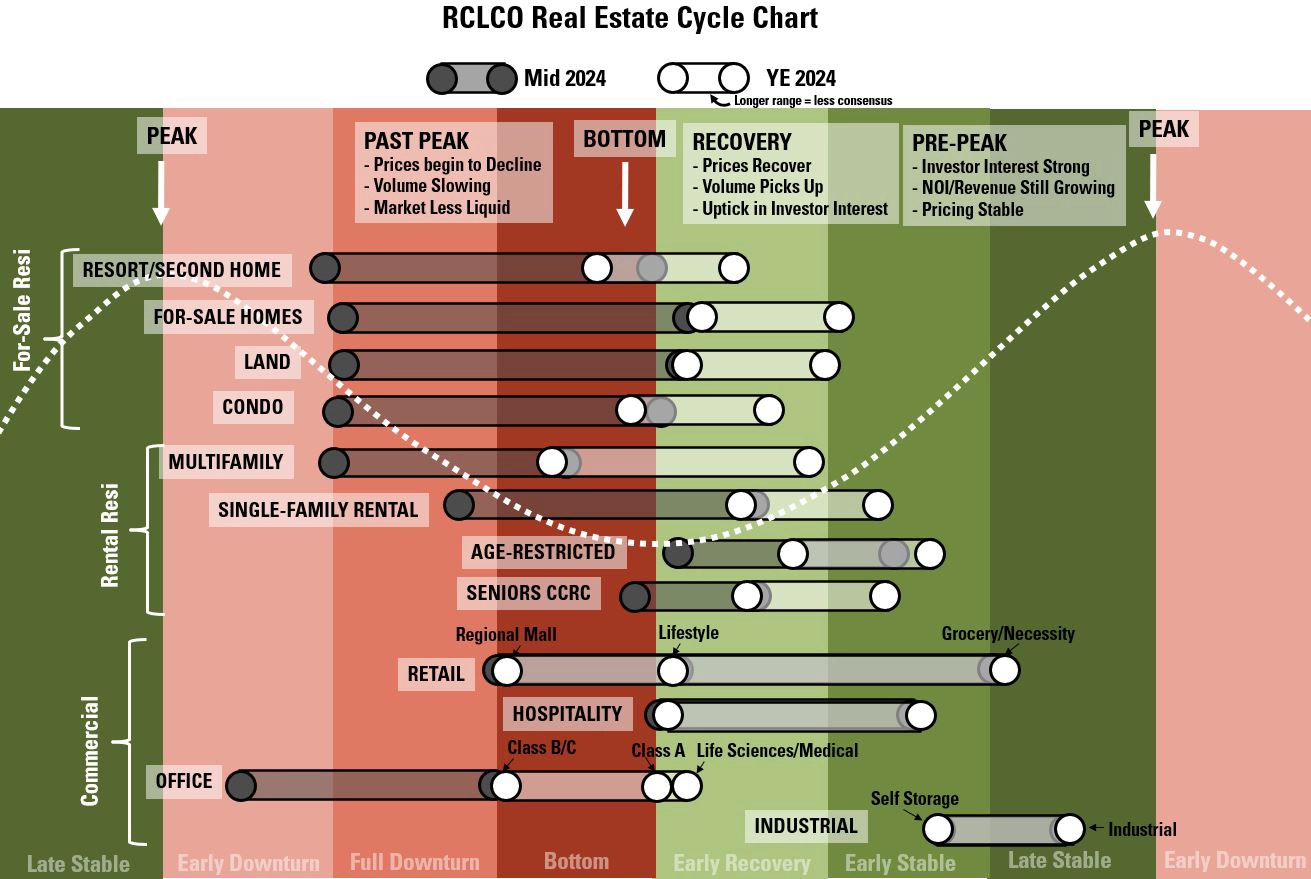

Moving into Expansion

At year-end 2024, many sectors have started to move into early recovery. As with our previous surveys, we reflect the range of responses (when there is less consensus) in the chart below – the longer the bar, the larger the variation in responses. Commercial uses often have more variation since they contain more subsectors of varying performance than the residential groupings, and that detail is labeled on the chart. Sentiment around the for-sale residential sectors showed signs of improvement – for-sale homes and land/lots are moving into early recovery. Sentiment around second home and condo was more mixed – but appears to be on the borderline of downturn and moving into early recovery. Multifamily rental sentiment was also somewhat mixed, but appears to be emerging from downturn, while subsectors such as single-family rental, age restricted, and seniors housing are in early recovery. Industrial remains stable, and hospitality continues to emerge into recovery. Retail shows more variation as grocery/necessity retail remains resilient, malls are in downturn, and lifestyle retail shows signs of recovery. Respondents indicated that Class A, and Class B/C office are currently in downturn, but Life Sciences/Medical may be moving into early recovery.

Cycle Stage Movement over Past Six Months

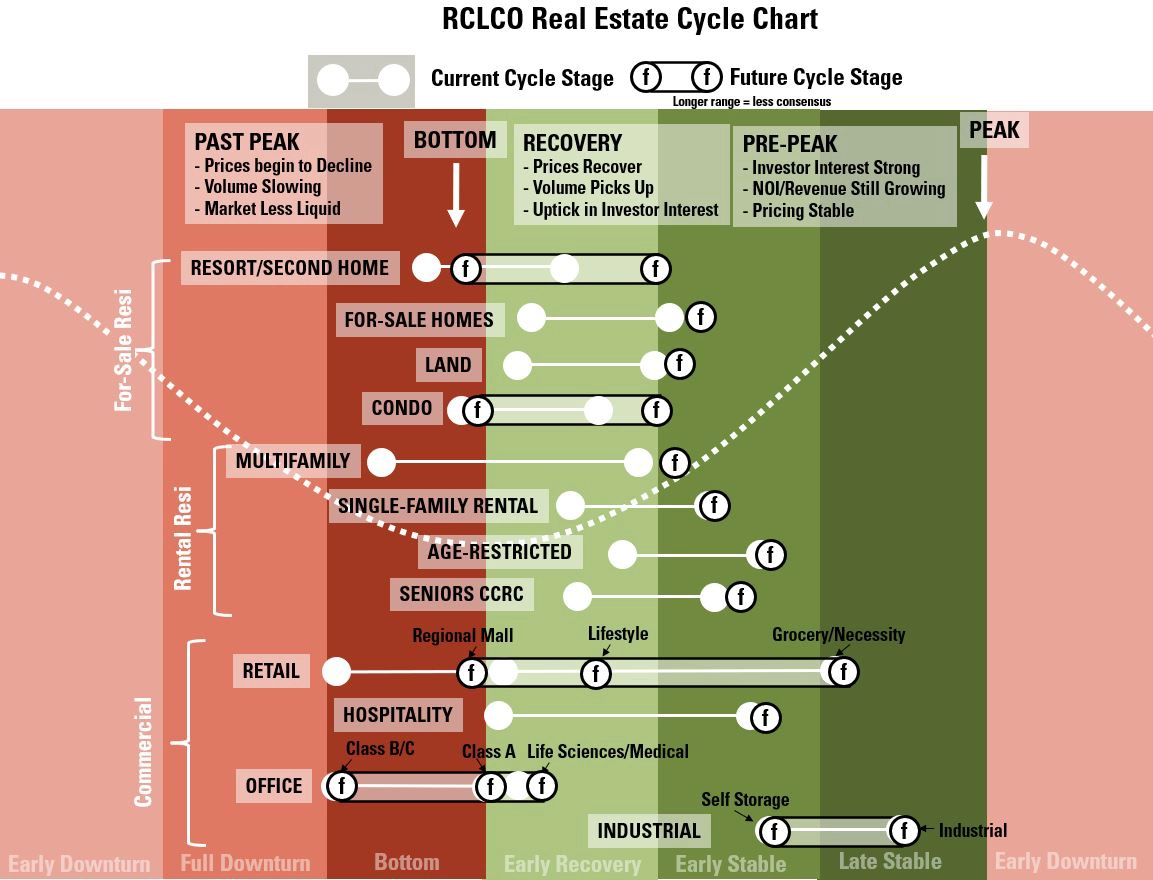

The Future Looks Bright

Looking forward, many of the residential sectors are moving into early recovery or early stable phases. The for-sale sectors have some variation with interest rates still high, and the condo and second home markets seem slowest to recover. The outlook for commercial sectors is also increasingly positive as hospitality, grocery-anchored retail, lifestyle retail, self-storage and industrial, and life sciences and medical office are expected to either remain stable or move into early recovery or early stable phases. Like at mid-year, the sentiment remains consistent that recovery in sectors such as traditional office and regional malls is expected to lag behind other sectors, remaining in downturn in the coming year.

Economic Indicator Predictions for the Next Year

Generally speaking, respondents expect key indicators that have an impact on real estate to continue improve at a moderate pace/rate.

What Do You Expect to Happen with the Following Economic Indicators Over the Next 6 to 12 Months Nationally?

Source: RCLCO

- The majority (66%) of respondents said that interest rates will decrease at a moderate pace, and 21% predict that interest rates will remain the same. This is a continued improvement in sentiment from mid-year, but again, predates the Fed’s announcement of only two cuts in 2025.

- Respondents feel cap rates will stay the same (40%) or decrease moderately (37%). This is significantly more consensus than at mid-year, when equal numbers believed cap rates would increase as those who believed cap rates would decrease.

- Inflation had less consensus than at mid-year – which roughly equal shares believing it will increase as the share predicting a decrease, though the largest share thinks they will remain stable (38%).

- In an increase in sentiment, the majority of respondents (68%) now believe that capital flows to real estate will increase.

- Views on construction costs were somewhat more pessimistic than at mid-year with 57% predicting an increase.

- The homeownership rate was predicted to increase moderately by 32% of respondents, a larger share than at mid-year.

Because it has a big impact on real estate valuation and debt costs, where do you think the 10-year treasury will be 24 months from now?

Source: RCLCO

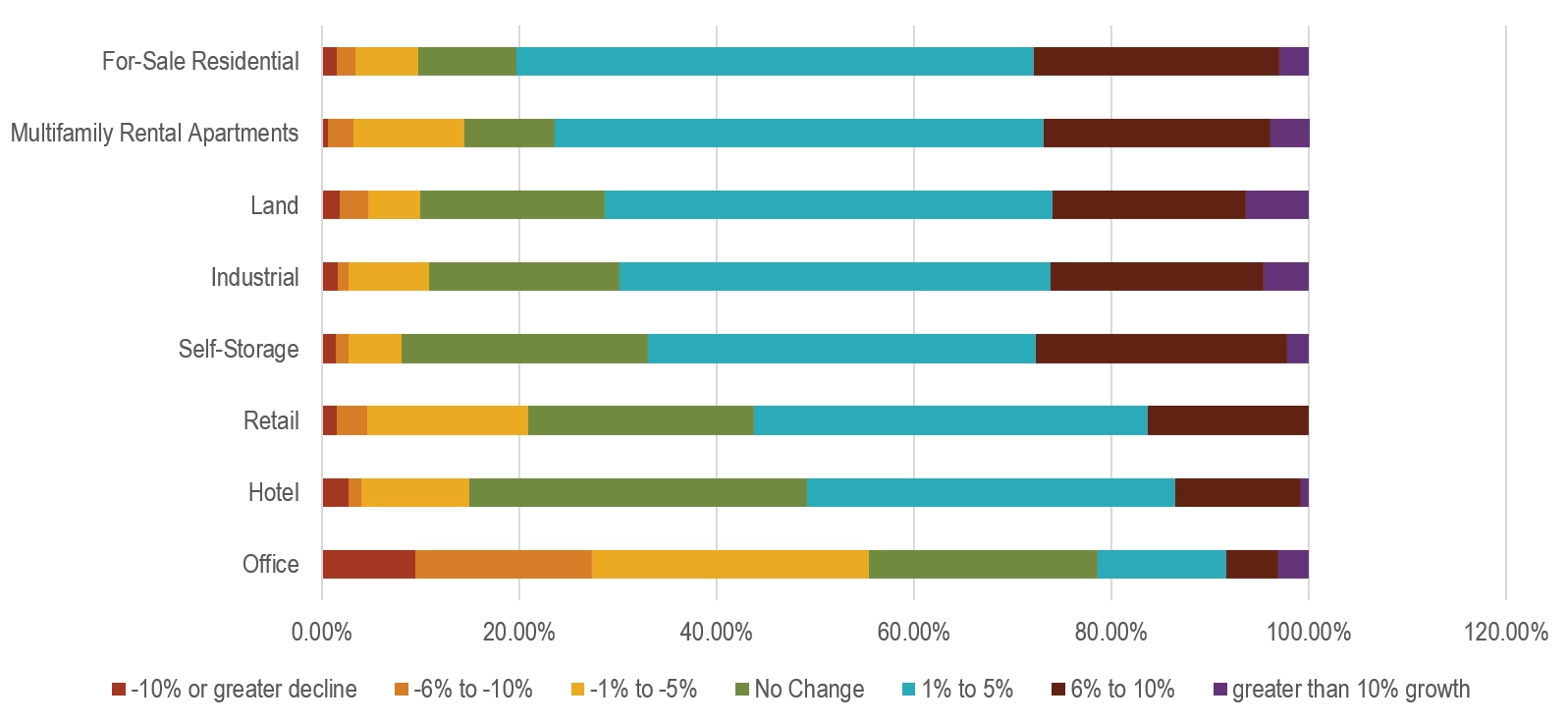

There was a mix of opinions on valuation changes for the following real estate sectors over the next two years. Encouragingly, all sectors except office are predicted to increase in value, with for-sale residential, multifamily, land, industrial and self-storage predicted to grow by a weighted value of 3.0% to 3.5%. Hotel and retail had more modest growth predicted, with a weighted value of approximately 1.5%, and office was predicted to decline in value by -2.25%.

How Much Do You Think Values will Change Over the Next 2 Years in the Following Real Estate Sectors?

Source: RCLCO

RCLCO POV

Q4 2024 – Real Estate is Poised to Emerge from Its Recession, But Significant Downside Risks Remain Regarding Inflation and Labor Market Conditions

In welcome news to real estate market participants, the Fed has now cut interest rates by a full percentage point since September, dropping to the 4.25% – 4.50% range, a two-year low. Indicating it was a close call as to whether to continue to drop rates in December, Fed Chair Jerome Powell said that the Fed will “be more cautious as we consider further adjustments to our policy rate.” New projections show officials expect to make fewer rate reductions next year, with most penciling in two cuts for 2025 if the economy grows steadily and inflation continues to decline. Previously, officials had penciled in four cuts for 2025.

While the risk of a downturn seems to be receding, a shallow recession is still possible (~20% probability), with further credit problems or an escalation of geopolitical conflict as possible triggers. After strong jobs growth all year, the employment market remained resilient adding 227,000 additional jobs in November, and the unemployment rate remained steady at 4.2%. The inflation outlook remains uncertain and merits close attention, with immigration policy and the promise of higher tariffs raising the concern of return to higher inflation and labor shortages.

Real Estate Sectors and Capital Markets

The yield on the 10 Year US Treasury Note is up ~70bps since mid-September after trending down since its most recent peak back in May 2024, and we think that long-rates will settle in the 4.0% to 4.5% range. Many real estate market participants have indicated that another approximately 25 to 50bps drop in the Fed Funds Rate will once again make many real estate developments and investments that have been stalled over the past two years begin to pencil, and we expect to see a spike in real estate activity as a result.

Real estate fundamentals have generally softened in 2024 due to heightened supply, particularly for apartments and industrial, despite above average solid demand/absorption. Neighborhood and strip retail fundamentals have improved as new supply is minimal, while office has suffered from weak demand and continued new construction. Even with a more favorable interest rate environment, we expect office rents to decline for the next several years, contributing to a continued wave of defaults and distressed sales. The life sciences office/lab sector has cooled with the overall office market, but we expect this sector will be among the first to recover. We expect industrial and apartment fundamentals to turn the corner with lower vacancies and better rent growth in 2025. Variability in performance from market to market remains very high and careful local market analysis remains crucial.

Niche or specialty sectors continue to be the bright spot in the real estate market. NCREIF has recognized the growing importance of these property types by adding many to the NCREIF Expanded NPI. Within the new NPI, data centers, manufactured housing, student housing, and hotels have all posted positive total returns (compared to NPI of -3.3%) over the past year.

The real estate capital markets are showing early signs of a recovery, with a spike in CMBS issuance in the nine months of 2024. The debt markets have been more active in the second half of 2024 than expected earlier in the year. Average commercial mortgage rates were down slightly through September 2024 but have risen along with Treasuries since then. While fundraising remains difficult for real estate, there are increasing signs that equity commitments are increasing and will continue to grow into 2025.

Who Took the Survey?

RCLCO’s Real Estate Market Sentiment Survey tracks the sentiments of a highly experienced pool of real estate professionals from across the country and the industry. A majority (68%) of respondents have worked in the real estate industry for 20 years or more, with an average respondent tenure of approximately 25 years, and 82% of respondents are C-suite or senior executives in their organizations.

Years of Experience in Real Estate

Source: RCLCO

Position in Organization

Source: RCLCO

Type of Organization

Source: RCLCO

Developers and builders comprise the largest share of respondents, at 40% of the sample. Another 24% are investors or capital allocators, followed by 7% in design or architecture firms. The remaining 35% of respondents come from a variety of other types of organizations within the real estate industry and public sector.

Primary Region/Market

Source: RCLCO

The respondent mix is representative of the U.S. as a whole: however, it is weighted towards those who report working primarily in coastal and Sunbelt markets. This respondent mix reflects markets where there has been significant development activity in this cycle.

Sentiment Survey article and research prepared by Charles Hewlett, Managing Director; and Kelly Mangold, Principal. RCLCO Point of View prepared by Charles Hewlett, Managing Director.

References

[1] The Real Estate Market Index (RMI) is based on a semiannual survey of real estate market participants and is designed to take the pulse of real estate market conditions from the perspective of real estate industry participants. The survey asks respondents to rate real estate market conditions at the present time compared with one year earlier (Current RMI), and expectations over the next 12 months (Future RMI). The RMI is a diffusion index calculated for each series by applying the formula “(Improving – Declining + 100)/2.” The indices are not seasonally adjusted. Based on this calculation, the RMI can range between 0 and 100. RMI values in the 60 to 70+ range are indicative of very good market conditions. Values below 30 are typically coincident with periods of economic and real estate market stress/recession.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Copyright ©️ 2024 RCLCO. All rights reserved. RCLCO and The Best Minds in Real Estate are trademarks of Robert Charles Lesser & Co. All other company and product names may be trademarks of the respective companies with which they are associated.