June 28, 2021

RCLCO recently worked with the ULI Terwilliger Center for Housing to prepare Low-Density Rental Housing in America. The report highlights the emerging market segment of purpose-built and institutionally managed single-family rentals, including supporting demographic trends, an explanation of concepts and case studies, and operating metrics and conclusions.

This article summarizes some of the key topics of the ULI Terwilliger Center for Housing Report, including:

- Demographic trends and affordability challenges leading to growth in the institutionalization of purpose-built single-family rentals

- The evolution of the single-family landscape

- Differentiating characteristics of various build-for-rent concepts and product types

- Operating metrics and financials

- Implications and conclusions regarding the single-family rental sector

Tailwinds

The United States is home to a broad spectrum of households with diverse housing needs; however, new rental deliveries in the past decade have primarily consisted of large-scale multifamily communities. Development patterns over the past decade have responded to existing structural and regulatory challenges, and the availability of debt for conventional multifamily properties further exacerbated rental housing’s uniformity.

Demographic shifts including the millennial cohort moving into prime family formation ages are a primary driver for growth in lower-density housing types. Given the constrained housing market and rising construction costs, the decline in homeownership affordability is one of the most pressing challenges facing many Americans, driving additional demand toward low-density rental housing. Today, the median home price is 5.6 times higher than the median income in the U.S., a significant change from the average of approximately 4.0 from 1985 to 2000. Additionally, the COVID-19 pandemic has created financial hardship for millions of American households and many may remain in the rental housing market for an extended period in the years to come.

The demographic tailwinds, the impact of COVID-19, and growing affordability concerns, which are highlighted in ULI’s 2021 Emerging Trends, contribute to the rapid institutionalization of a new rental housing product type: purpose-built, single-family rentals. While single-family rental homes are not a novel concept, as households have rented single-family homes for decades, purpose-built, single-family rental homes are a relatively new concept.

Single-family rentals (“SFR”) benefit from the maturing millennials seeking a new type of rental product that matches their changing lifestyles, empty nesters looking to downsize to a maintenance-free living option, and the array of households in transitional life stages. Given the strong tailwinds for purpose-built, single-family rental housing, many new players have entered or are considering the purpose-built single-family asset type. Furthermore, given the organic growth of the product type over the past 10 years, there is a wide variety of products, communities, and strategies, which increases confusion across the industry and the media regarding nomenclature. RCLCO and ULI have set out to codify the single-family rental market’s language, product types, and differentiating characteristics.

Defining the Landscape

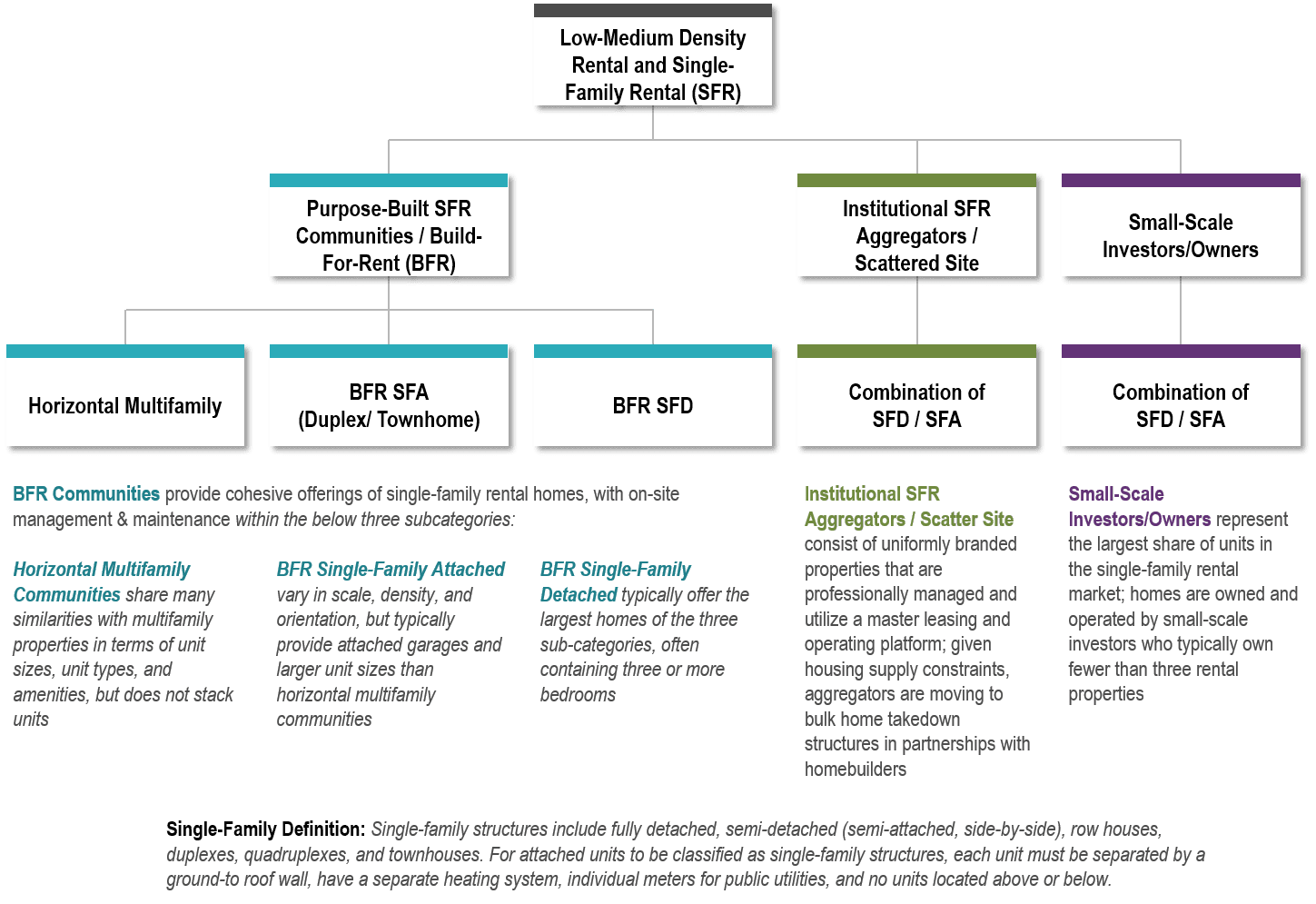

The competitive landscape for institutionalized SFR housing continues a rapid evolution as more companies enter the asset class, each with various strategies, product types, positioning, and locations. Despite the significant variation in offerings already in the market, most market participants agree on the asset class’s overarching term: single-family rentals.[1] However, less consensus exists on the subclassifications. RCLCO and ULI analyzed hundreds of news articles and conducted interviews with various market experts to attempt to codify the language around the product type, which is detailed in the chart below:

Small-Scale Investors/Owners represent more than 97% of the existing SFR housing market, generally owning only a few properties and listing on online marketplaces such as Zillow. After the Great Financial Crisis, Institutional SFR Aggregators emerged and aggregated thousands of homes across various markets, utilizing robust platforms and economies of scale. This group has also started to work directly with builders to purchase blocks of homes to add to their portfolio as the inventory of resale homes has tightened. The newest group is the Purpose-Built SFR or Build-For-Rent (BFR) Community, where the entire community is planned and built as rental, and thus has consistent branding, housing quality, and often offers on-site resources such as leasing services, property management, and amenities.

Build-for-Rent Concepts

Within the BTR space there are also more subtle product distinctions based on unit mix, product type, and other factors. Horizontal multifamily, comprised of dense Single-family Detached (SFD) units, can achieve densities of nine to 14 units per acre, include private lawns/patios and a clubhouse with pool, and attract older millennials (pre- or early-family), downsizing empty nesters, those newly relocating to a market, and divorcees. RCLCO determined that 75% of this product type has been developed as infill development in established suburban locations, with the balance occurring in rapidly growing greenfield suburbs. Horizontal multifamily fills a product gap between traditional single-family homes and garden-style multifamily apartments. It attracts households that prefer a single-family home’s privacy but do not need or cannot afford the large square footages of traditional single-family homes. The main competition to horizontal multifamily is garden-style apartments, with some competition from SFA and SFD homes on the shadow market, and because this type is generally preferred to the alternatives, it commands a substantial pricing premium on a size-adjusted per square foot basis. Despite premium positioning, smaller unit sizes at horizontal multifamily communities typically produce lower monthly rent payments than the monthly cost of ownership within the same submarket.

Private Backyard at Avilla Eastlake in Thorton, CO

Image Credit: NexMetro Communities

Build-for-Rent Single-Family Attached housing encompasses a broad spectrum of community configurations, unit types, and sizes, though each unit shares at least one vertical wall, and units are not stacked on top of each other. Because SFA communities are located in urban and suburban settings, they have noticeable variations in project sizes and types, with densities of between eight to 16 dwelling units per acre (communities offering three-story townhouses able to achieve relatively high densities). Units at SFA communities generally provide two or more bedrooms and are larger on average than multifamily unit sizes but smaller than traditional single-family homes. In urban locations, there may be limited amenities, but newer suburban communities may have a clubhouse and pool. The market audience also varies by location, with urban infill communities attracting more young professional couples and roommates and some empty nesters, and suburban locations attracting more relocating families and prefamily millennial couples. Given larger unit sizes and increased competition from the shadow market, BFR SFA communities are typically priced a slight size-adjusted premium over garden-style apartments, though premiums vary by quality and amenitization of the SFA community. Larger unit sizes and strong pricing typically yield monthly rent payments comparable to the monthly cost of ownership, assuming at least a 10 to 15 percent downpayment.

Pool Amenity at BB Living at Val Vista in Phoenix, AZ

Image Credit: BB Living Residential

Build-for Rent Single Family-Detached communities are the most similar to SFR units owned by institutional aggregators and small-scale investors but benefit from economies of scale with high concentrations of units in a single location and cohesive branding. Many of these communities are associated with or are sold from a larger master-planned community and have an average density of three to seven dwelling units per acre.

- Given these lower densities, SFD communities are predominantly located in suburban locations and are typically platted as individual residential lots.

- Units at SFD communities generally provide three or more bedrooms and are significantly larger on average than multifamily unit sizes, and have large fenced backyards.

- Higher-end communities also typically have a pool and clubhouse, and those that are located within an MPC also are allowed access to the broader community amenity center.

The primary audience for BFR SFD homes is family households, typically in a transitional period after moving to a new market or during home construction, with mature professionals and empty nesters representing secondary market audiences. The majority of SFD communities are located in greenfield suburbs and the primary competition is inventory owned by institutional aggregators or small-scale investors. BFR SFD communities are typically priced at a slight size-adjusted premium over garden-style apartments, but at healthy premiums over small-scale investor inventory, given the elevated level of execution, on-site property management, yard maintenance, and amenities provided by the BFR communities. Larger unit sizes and strong pricing typically yield monthly rental payments comparable to the monthly cost of ownership, assuming a downpayment ranging between 10 and 15 percent.

Typical Street and Housing Types at Pradera in San Antonio, TX

Image Credit: AHV Communities

Operating Metrics

Property characteristics, target demographics, and locations vary across the SFR product classifications, resulting in differing project economics. Development patterns in recent years help illustrate the possible supportable land values, operating expenses, and investor appetite for the evolving land use. Density is often the most significant variable driving achievable land values, with horizontal multifamily able to pay higher land values in suburban infill locations due to their density, while BFR SFD typically compete with single-family for-sale developers in more suburban lower-density locations. Compared to traditional multifamily products, SFRs have historically enjoyed lower turnover because of “stickier” occupancy, lower overall maintenance costs due to limited common areas, and more upside in asset values. As a tradeoff, SFR investments require higher long-term capital expenditure requirements and upfront rehab costs (for existing homes). Historically, SFRs have achieved cap rates 20 to 50 basis points higher than garden-style apartments, but competition from potential investors has driven yields downward in the past year, with single-family cap rates now in line with traditional garden-style multifamily communities.

Implications and Conclusions

SFR housing has played an essential role throughout history in America, as large swaths of the U.S. population seek rental housing options other than high-density, multifamily properties. The trend toward purpose-built SFR housing has evolved over the past decade but has experienced exponential interest and growth over the past few years. As for many long-term trends, the outbreak of COVID-19 exacerbated and emphasized the need for a broader diversity of rental housing. Many of the key trends outlined in ULI’s 2021 Emerging Trends in Real Estate report, including the rise of working from home, a geographic shift to more affordable Sunbelt markets, growing demand in suburban neighborhoods, and the substantial and growing affordability crises, provide support for the investment thesis behind much of the growth in low-density rental housing.

The expansion and capitalization of low-density rental housing can deliver more housing at price points below the cost of purchasing homes within a respective neighborhood. However, there are some concerns that the institutionalization of the SFR housing market could have some unintended, adverse effects on affordability and equity issues unless public policy and developer responses address them as outlined in the report. While it is unlikely that low-density rental housing will solve the country’s substantial affordability crises, providing more housing alternates to meet the needs of a diverse array of American households is a positive step forward. For more detail on the topics discussed in this summary, please read the full article by clicking here.

Article and research prepared by Todd LaRue, Managing Director, and Cameron Pawelek, Vice President. Additional research and support provided by Ryan Guerdan, Senior Associate, and Liam Mercer, Analyst

[1] Single-family structures include fully detached, semi-detached (semi-attached, side-by-side), rowhouses, duplexes, quadruplexes, and townhouses. For attached units to be classified as single-family structures, each unit must be separated by a ground-to-roof wall and have a separate heating system, individual meters for public utilities, and no units located above or below.

Top image courtesy of BB Living and Mark Taylor

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.